The Lemonade Paradox: A Near-Perfect Business Story With One Glaring Problem

The growth is real, the founders are credible, and the market is enormous. So why isn't it a buy yet?

Insurance is one of the oldest, least-loved industries in the world. Lemonade set out to fix that in 2015 with a simple idea: use AI, remove the conflict of interest, and build something customers might actually trust. A decade later, the growth numbers are hard to argue with. The AI thesis is starting to show up in the margins. The founders are still at the wheel. And yet, for all the things going right, one stubborn financial reality is keeping this stock out of the buy column. Here is our full breakdown.

The Founding Story

In 2015, Daniel Schreiber and Shai Wininger sat down to redesign insurance from scratch. Schreiber was a tech executive. Wininger had co-founded Fiverr. Neither had worked in insurance a day in their lives, and that was entirely the point.

What bothered them wasn’t the premiums. It was the conflict of interest baked into every traditional insurance company. Every dollar paid in claims is a dollar taken from profit. The incentive to deny is architectural. Customers know this, which is why insurance consistently ranks among the lowest-trust industries in the world.

Their answer was the Giveback model. Lemonade charges a flat 20% fee to cover operating costs. The rest pools for claims. Anything left at year-end goes to a charity of the customer’s choosing. Profit comes from fees and investment income, not from denying claims. The conflict is structurally removed.

They launched in New York in 2016, selling renters insurance at roughly a third of incumbent prices, with claims handled in minutes by AI. The product went viral in a way insurance never had before. Word spread that it actually worked.

By 2020, they were public on the NYSE. The stock soared, then crashed, along with every other high-growth name, as losses widened in 2022. At its trough, LMND traded below $12. In 2026, with losses narrowing sharply and growth accelerating, the story looks considerably more interesting again.

What Lemonade Does and How It Makes Money

Unlike most insurtechs, which are really just distribution middlemen, Lemonade is a full-stack carrier. It holds its own licenses, takes the underwriting risk, and pays the claims. It is a real insurance company. It just doesn’t look like one.

The experience is entirely app and web-based. A renters policy takes about 90 seconds. Claims are described in plain language, a photo is uploaded, and in straightforward cases, the AI approves and pays in minutes. The company once settled a claim in 3 seconds.

The product lineup spans renters, homeowners, pet, car (growing roughly 40% year-over-year, with a Tesla FSD partnership launched in 2026), term life, and a rapidly expanding European operation that grew in-force premium (IFP) by over 200% year-over-year.

The business model shifted significantly in mid-2025. Lemonade had historically ceded around 55% of premiums to reinsurers, keeping only 45% of the economics. Confident in its AI underwriting, it cut that cession to around 20%, retaining 80% of premium economics. That single shift is worth an estimated $30M in annual savings and has driven a step-change in reported margins. In Q1 2026, revenue grew 71% year-over-year to $258M, while gross profit jumped 159% to $100M.

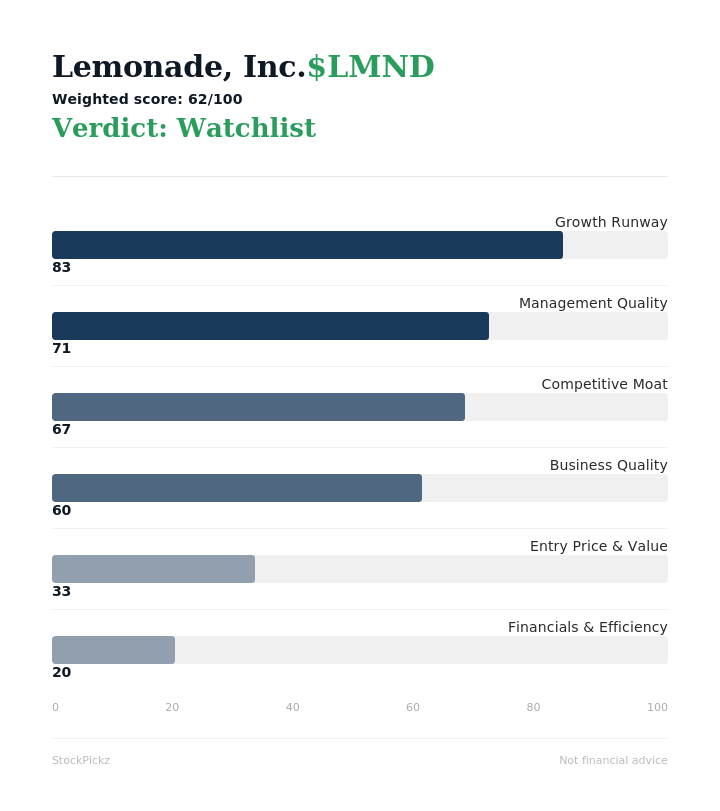

Competitive Moat: A Real Edge, Still Being Sharpened

The moat is real but still maturing. Ten years of proprietary AI training data across underwriting, pricing, and claims is not something a competitor can replicate quickly. The AI improves claim selection accuracy by roughly 30%, and Lemonade has maintained a 3:1 LTV-to-CAC ratio even as marketing spend tripled. That is the signature of a machine getting smarter, not just bigger. An 85% annual dollar retention rate, improving year over year, is the most direct evidence of genuine customer stickiness.

The moat has structural breadth too: brand differentiation through the Giveback model, switching costs as customers bundle multiple products, and early-stage data network effects. What holds the score back is unproven pricing power. Lemonade has improved its economics through better underwriting, not through raising prices. There is also limited evidence of organic word-of-mouth growth at scale.

Management Quality: Founders Still in the Cockpit

Schreiber and Wininger have been co-CEOs for ten years. Founder-led, long-tenured, meaningfully equity-aligned, and not net sellers. But what distinguishes this management team most is the quality of their communication. Their shareholder letters are among the most candid in the sector. In 2022, they publicly set a target for adjusted EBITDA profitability by late 2026. In Q1 2026, they are tracking exactly to that timeline.

Capital discipline has been real. Non-growth operating expenses have been essentially flat for three years while the business doubled. The company reached $1M of IFP per employee in Q1 2026, nearly three times its 2022 figure. The primary gaps are an executive pay structure not clearly tied to long-term return targets, and insufficient data to confirm a strong internal culture rating.

Business Quality: The Model Works, Not Yet Confirmed

Insurance is a structurally attractive business model. Premiums are recurring, habitual, and paid upfront. Lemonade’s 85% annual dollar retention confirms that holds in practice. The gross margin trajectory is striking: from 19% in 2023 to 41% in Q3 2025 and 48% in Q4 2025. However, Q1 2026 slipped back to 39%, a reminder that quarterly margins in insurance are sensitive to loss timing and catastrophe events. The 40% threshold has not been confirmed as a consistent baseline yet.

The business will clearly exist and matter in ten years. AI-native insurance delivery will be more relevant in a decade, not less. What drags the score is the cash flow history. GAAP operating cash flow only turned positive in 2025, and capex discipline has not been confirmed across multiple years.

Growth Runway: The Market Is Enormous and Barely Touched

The strongest area of the analysis. The U.S. property and casualty market alone is roughly $900 billion. Lemonade’s $1.33 billion in IFP represents less than 0.2% penetration. The opportunity is not a concern. It is one of the most compelling parts of the thesis.

The runway has multiple distinct vectors: car insurance expanding state by state, European operations up over 200% year-over-year, pet insurance now the company’s largest line, and cross-sell bundling compounding with 18% of IFP now coming from bundled customers at near-zero acquisition cost. The Tesla autonomous vehicle partnership adds long-duration optionality. The one genuine risk is climate. Catastrophic weather is a structural headwind for homeowners underwriting that technology alone cannot fully solve.

Financials and Efficiency: The Numbers Have Not Caught Up Yet

This is where the analysis hits its hardest wall. Return on invested capital is -12%. Return on equity is -29%. These are not trivial misses. They indicate the company is still consuming capital faster than it generates returns on it, and a score this low is enough to cap the overall business grade regardless of how strong everything else looks.

Context matters. Five years ago, ROIC was -292%. Net loss in Q1 2026 was $36M versus $62M a year prior, while revenue grew 71%. EPS losses are narrowing fast. Revenue is growing while non-growth operating expenses decline. The AI leverage is real and visible in the numbers. But it takes more than a compelling trajectory. It takes confirmed, sustained positive returns. Positive adjusted EBITDA in Q4 2026 and GAAP profitability in 2027 are the milestones that will change this picture.

Entry Price and Value: Growth Already Priced In

At roughly $55, LMND trades at about 4.87x forward price-to-sales. Traditional insurers trade at 1-2x revenue. The premium the market is paying is an explicit bet that Lemonade becomes a technology company that sells insurance, not an insurance company that uses technology. The bull case requires sustained 30%+ growth and meaningful margin expansion over multiple years, leaving little room for error.

Two things temper the concern. The stock has already fallen roughly 45% from its 52-week high of $100, pricing out some of the earlier froth. And with no GAAP profits yet, anchoring a precise fair value requires so many assumptions that the exercise is more art than science. For a long-duration investor, valuation is the least important dimension here. The financial fundamentals are the real gating factor.

Final Verdict

Lemonade passes every qualitative test: credible founders, clean incentives, genuine product innovation, a massive market, and multiple visible growth vectors. It fails the primary quantitative test of sustained positive returns on invested capital. The weighted score of 62/100 puts it on the “Watchlist” for me. Until the company can improve its financials and efficiency, I’m sitting on the sidelines.

Great stories and great investments are not the same thing until the economics confirm each other.

For informational purposes only. Not financial advice.