The Delivery Giant Nobody Expected to Win

A Deep Dive into DoorDash.

Everyone wrote off DoorDash (NASDAQ: DASH).

At its IPO in December 2020, one analyst called it “the most ridiculous IPO of 2020.” The company had lost $667 million in 2019, operated in a brutally competitive industry, and had no clear path to profitability.

Fast forward to today: DoorDash commands over 60% of the U.S. food delivery market, operates across 40+ countries, generated nearly $14 billion in revenue in 2025, and posted $935 million in GAAP net income, proving the economics actually work.

The question now isn’t whether DoorDash can survive. It’s whether it can build something durable.

The Business: Delivery Was Just the Entry Point

At its core, DoorDash is a three-sided marketplace connecting consumers, merchants, and Dashers (delivery drivers). But wise investors would tell you to look past the surface.

What DoorDash is actually building is a local commerce platform. The infrastructure layer for anything moving from a merchant to a consumer quickly. Restaurants were just the beachhead. Today, about 30% of U.S. monthly active users order from non-restaurant categories: groceries, alcohol, pharmacy items, and retail goods. The more use cases it owns, the stickier it becomes.

How it makes money: Merchant commissions (15–30% per order) drive roughly 55–60% of revenue. DashPass subscriptions at $9.99/month and 22+ million members generate recurring, predictable revenue Buffett would appreciate. Advertising (merchants paying for promoted placements) doubled year over year and is becoming a high-margin engine that most investors are underpricing.

The Amazon playbook: build the marketplace, then sell access to it.

The Growth: Proving the Bears Wrong

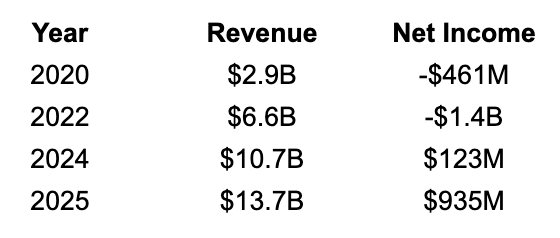

DoorDash’s revenue growth and net income growth don’t lie. Take a look at the numbers:

Revenue grew 4.7x since the IPO. Net income swung from deep losses to nearly a billion dollars, a 660% jump in a single year. Total orders crossed $100 billion annualized globally. The stock, meanwhile, pulled back nearly 45% from its October 2025 high of ~$285, then recently resumed its uptrend from its low.

The business is quietly becoming what the bears said it couldn’t be.

The Bull Case

I love to see obvious businesses in large markets that are hard to replicate. DoorDash is starting to check those boxes.

The U.S. flywheel is real: more orders → more Dasher supply → faster delivery times → more consumers → more orders. That virtuous cycle has widened the gap against Uber Eats and Grubhub, not narrowed it.

The international opportunity is large. The 2025 acquisition of Deliveroo for ~$3.85 billion now puts DoorDash across 40+ countries, serving more than 1 billion people. Food delivery penetration in Europe and Asia trails the U.S. significantly — that’s runway, not saturation.

The path to $25B+ in revenue by 2029 doesn’t require heroic assumptions. At 28% growth in 2025, the trajectory is credible.

The Bear Case

Munger always asked: “Tell me where I’m going to die, so I don’t go there.”

The moat question is the big one. DoorDash’s advantages (scale, brand, DashPass loyalty) are real but not invincible. Unlike a Coca-Cola or a toll bridge, DoorDash is fighting for every order in a commoditized category. If Uber Eats offers a better deal tonight, you switch tonight.

Capital intensity is a concern. Buffett avoids businesses requiring constant reinvestment just to stay competitive. DoorDash is guiding for several hundred million dollars of incremental 2026 investment to integrate three platforms (DoorDash, Wolt, Deliveroo) and scale autonomous delivery, on top of the $3.85B already spent on Deliveroo. UBS recently downgraded DASH for exactly this reason: synergies are being reinvested rather than flowing to shareholders.

Valuation is unforgiving. At roughly 85-90x earnings, the stock is priced for perfect execution. Any stumble, such as integration delays, consumer spending slowdowns, competitive fee pressure, and the multiple compresses fast.

Regulatory headwinds won’t go away. Gig worker classification battles in California, the EU, and Australia all add operating cost risk that’s difficult to model. Not existential, but a recurring tax on margins that a truly wide-moat business wouldn’t face.

The Verdict: Watchlist, Not Buy List

DoorDash is not a classic Buffett stock. It requires ongoing capital investment, operates in a competitive marketplace, and trades at a premium multiple that leaves little margin for error.

But here’s the tension: the stock is down 33% from its highs while the business accelerated. Revenue grew 28%. Profits surged 660%. That kind of disconnect between stock price and business performance is exactly what Lynch told investors to pay attention to.

The question is whether the investments being made today (the global platform, autonomous delivery, the advertising engine) will produce something more defensible tomorrow. If yes, this is a compounder. If no, you’re paying a growth multiple for a logistics company without a true moat.

My take: The business has earned credibility. The stock, after the pullback, is becoming interesting. But before this makes the buy list, I want to see the Deliveroo integration execute cleanly, margins improve on a sustained basis, and the advertising business scaling faster than the market appreciates.

When those boxes start getting checked, that’s when this becomes a real conversation.

The story isn’t over. It’s just entering its most important chapter.